How To Create A Profit And Loss Statement On Excel

We may receive compensation from partners and advertisers whose products appear here. Compensation may impact where products are placed on our site, but editorial opinions, scores, and reviews are independent from, and never influenced by, any advertiser or partner.

Designed to provide business owners with revenue and expense details, the profit and loss statement, or P&L statement, is a must for business owners, whether you're a small business bookkeeper, or the head of a global conglomerate.

Overview: What is a profit and loss statement?

Like a cash flow statement, a profit and loss statement provides you with detailed information regarding both revenues and expenses for your business.

Also known in accounting terms as an income statement, even a basic profit and loss statement can provide you with a convenient window through which you can view your company's revenue and expenses.

In addition, profit and loss statements can also be a useful tool for creating a budget or calculating your working capital.

How to write a profit and loss statement

It's up to you how frequently you wish to run a profit and loss statement. Some companies choose to run one monthly, while others prefer quarterly profit and loss statements.

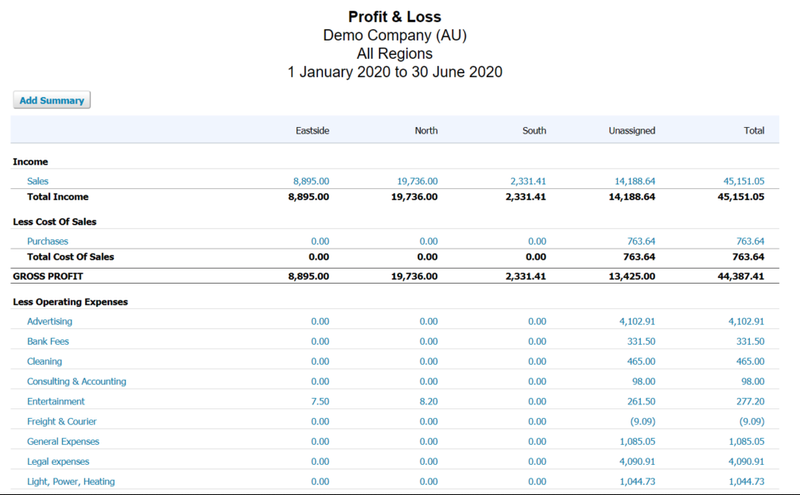

Example profit and loss report comparing a company's P&L in four regions. Source: beanninjas.com.

Whatever your preference, the best way to create a profit and loss statement is by using accounting software, which will take care of the entire process for you. If you currently do not use accounting software, you can use a template to create a profit and loss statement.

Here are the steps to take in order to create a profit and loss statement for your business.

Step 1: Calculate revenue

The first step in creating a profit and loss statement is to calculate all the revenue your business has received. You can obtain current account balances from your general ledger such as cash and current accounts receivable balances.

If you're creating a monthly profit and loss statement, you'll include all of the revenue received in that time frame, whether your business has collected that revenue or not. If you've chosen to run a quarterly statement, just add up the revenue received in that three-month time frame.

When calculating revenue, be sure to include all revenue received, whether it's from selling products and services or from selling your old printer to the business next door.

Step 2: Calculate cost of goods sold

Your cost of goods sold is an important part of any profit and loss statement. If you're selling wallets, you'll have to include the cost of purchasing the wallets from the manufacturer.

If you're making the wallets, you'll have to include the materials and supplies needed to make them. If you're selling services, you need to include the cost of your time or your employee's time that provided the service.

Step 3: Subtract cost of goods sold from revenue to determine gross profit

Once you have calculated your revenue and your cost of goods sold, you'll just need to subtract the cost of goods sold to arrive at your gross profit number. Gross profit is the profit your business has earned from selling your products and/or services.

Revenue - Cost of Goods Sold = Gross Profit/Loss

Step 4: Calculate operating expenses

The next thing you need to do is calculate all of your operating expenses. Operating expenses include rent, travel, payroll, equipment, utilities, and postage.

Step 5: Subtract operating expenses from gross profit to obtain operating profit

Once your operating expenses have been calculated, you'll want to subtract that total to obtain your total operating profit. This will give you your total operating profit or loss.

Gross Profit - Operating Expenses = Operating Profit/Loss

Step 6: Add additional income to your operating profit

If you have any additional income not included in your revenue totals above, such as interest income or dividends from investments, you'll want to include them here. Once added to your operating profit, the total is earnings before interest, taxes, depreciation, and amortization, otherwise known as EBITDA.

EBITDA = Operating Profit + (Interest Income + Dividends Earned)

Step 7: Calculate interest, taxes, depreciation and amortization

The next step is to calculate any interest payments, taxes due, as well as depreciation and amortization expenses.

Step 8: Subtract interest, taxes, depreciation, and amortization expenses from EBITDA to obtain net profit

Your final step is subtracting interest, taxes, depreciation, and amortization expenses to arrive at your net income, or net profit.

Net Profit/Loss = EBIDTA - (Interest + Taxes + Depreciation)

What does a P&L statement tell you about your business?

A profit and loss statement lets you know exactly how your business is doing. Often used to determine both strengths and weaknesses in businesses, a profit and loss statement can also tell you the following:

Whether your products or services are profitable

We're all in business to make a profit, so it's no surprise that one of the most important markers for your business is your gross profit. Your gross profit is calculated by subtracting the cost of goods sold from revenue earned.

This number can tell you how well your products are performing or whether your services are profitable. If your gross profit is low, look to increasing sales.

Whether your business is trending in the right direction

When reviewing your profit and loss statement, it's important to look at trends. Whether you calculate profit and loss on a monthly or quarterly basis, comparing reports can help you understand exactly how your business is trending.

For instance, if your net profit for January was $11,000, but dropped down below $5,000 in February, March, and April, you'll need to do a deep dive into your business finances to determine what happened. You can do that by first examining gross profit. If gross profit is down, your course of action should be to increase sales.

However, if gross profit has remained consistent but net profit is down, that signifies an increase in operating expenses, so you'll want to start looking at ways to cut expenses. While one profit and loss report is helpful, comparing them can be even more helpful.

How healthy your business is overall

The bottom line. When you hand over financial documents to investors or financial institutions, their eyes go to the bottom line: net profit. While having a loss isn't the end of the world, it does signify that something is amiss, either as a one-time issue or across business operations.

Either way, the profit and loss statement lets you see exactly where your business stands in terms of profit, which in turn allows you to make better business decisions.

Best accounting software to create a profit and loss statement

It's not difficult to find a profit and loss statement template that can be used to create a simple profit and loss statement, but the entire process is much easier if you use accounting software.

By tracking the information needed to create a profit and loss statement such as revenues and expenses using accounting software, you can have a current profit and loss statement in seconds.

1. QuickBooks Desktop

QuickBooks Desktop is one of the best accounting software options for small and growing businesses. Offering three plans, you can easily scale up to the next plan as your business grows. The latest version of QuickBooks Desktop offers enhanced system navigation and expanded help options.

QuickBooks Desktop offers a good selection of profit and loss statements for your business.

QuickBooks Desktop offers top-notch reporting capability, including several variations of the profit and loss statement. Reports can be easily customized and exported to Microsoft Excel for further customization if needed.

QuickBooks Desktop offers three plans:

- Pro: The Pro plan is $299.95/year and supports up to three users.

- Premier: The Premier plan also includes industry-specific reporting options. It's priced at $499.95/year and supports up to five users.

- Enterprise: Enterprise is the best plan for actively growing businesses. It costs $849.10/year and supports up to 30 users.

2. FreshBooks

FreshBooks is a small business accounting application that offers a long list of features geared toward sole proprietors and very small businesses. Offering online access as well as a mobile app for both iOS and Android devices, Freshbooks lets you collaborate with your employees, contractors, and accountants.

FreshBooks offers profit and loss statements by month or by quarter.

Even sole proprietors need to know how profitable their business is, and FreshBooks does a good job of providing business owners with the reports they need to make good management decisions.

FreshBooks offers four plans, all include product support and solid reporting capability:

- Lite: The Lite plan is $15/month and supports up to 5 billable clients.

- Plus: The Plus plan runs $25/month and supports up to 50 billable clients.

- Premium: Premium is $50/month and supports up to 500 billable clients.

- Select: The Select plan is custom-priced and supports more than 500 billable clients.

3. OneUp

OneUp is an affordable, easy to use accounting software application well suited for sole proprietors, freelancers, and small business owners. Offered on the cloud, OneUp works on desktop systems, laptops, and all mobile devices.

OneUp includes a profit and loss statement on their financial dashboard.

A OneUp feature that sets it apart from the competition is the option to enter transactions manually or connect to a bank for automatic transaction posting. Great for smaller businesses, OneUp includes a financial dashboard that provides you with a good view of business profit and cash flow.

OneUp's pricing structure is also unique, with all features included in all plans, plan pricing based on the number of system users, with five options available:

- Self: For single users, the Self plan is $9/month with no product support

- Pro: Supports 2 users and runs $19/month with unlimited support

- Plus: Supports up to 3 users and runs $29/month with unlimited support

- Team: Supports up to 7 users and runs $69/month with unlimited support

- Unlimited: For 8 or more users, Unlimited runs $169 per month with unlimited support

For a more complete list of accounting software applications, be sure to check out The Blueprint's accounting software reviews.

A final word about the profit and loss statement

Creating a profit and loss statement for your small business is vital since it's one of the best reports to determine whether your business is profitable.

Required by lending institutions and investors alike, a profit and loss statement can also help you pinpoint areas of success as well as spots where your business may need additional help.

The Motley Fool has a Disclosure Policy. The Author and/or The Motley Fool may have an interest in companies mentioned.

How To Create A Profit And Loss Statement On Excel

Source: https://www.fool.com/the-blueprint/profit-and-loss-statement/

Posted by: weidmanatudeas.blogspot.com

0 Response to "How To Create A Profit And Loss Statement On Excel"

Post a Comment